Disclaimer

The results obtained from these calculators are for general purposes only to illustrate the effect of compound interest and are not intended as a substitute for professional financial advice. Before making any financial decisions on the basis of these results, you will need to consult with an independent financial planner or accountant as well as consider whether the advice is suitable to meet your personal financial objectives and circumstances.

The actual performance of any investments will depend on future economic conditions, investment management, fees and taxation. Past performance is no guarantee of future performance and as a result of this, all the results are hypothetical and are NOT GUARANTEED.

Nambawan Super specifically disclaims any liability for any direct, indirect, incidental, consequential or special damages arising out of or in any way connected with the access to or use of these calculators. To the extent permitted by law, under no circumstances will Nambawan Super be liable for any loss or damage caused by a user's reliance on the information by using these calculators.

Assumptions

Projected super balance at retirement:

The projected total super balance takes into account your starting balance, employee and employer contributions, any additional voluntary contributions as well as interest earned between now and your retirement.

Retirement age:

We have assumed a default retirement age of 65. This can be adjusted in the calculator.

Working life:

The calculator assumes that you will have a continuous working life with no breaks up to your retirement age.

Interest rate:

The default investment returns have been set at 6.0%. This is based on the Nambawan Super 10-year average interest rate.

Employee contributions:

PNG Superannuation laws dictate that 6% is the mandatory minimum contribution for employees to make. Employees may choose to contribute more than the minimum.

Employer contributions:

PNG Superannuation laws dictate that 8.4% is the mandatory minimum contribution that employers have to make. Employers may choose to contribute more than the minimum.

Background on tax systems

Taxation is an important way that the government raises money to spend on goods and services needed by the people.

In developing countries like Papua New Guinea (PNG), the tax system relies heavily on 12% of its population of ‘lower-to-middle’ income earners but its benefits are shared widely to 88% of the population, who are mostly subsistence farmers living in rural areas.

PNG has a high rural-to-urban population ratio. This means that the minority of the formally employed income earning population have to pay high tax to the Government to enable it to spend on goods and services for all its citizens. Ideally, the tax system should raise the Government’s revenue without overburdening its population. Elsewhere, in more developed economies where tax systems are supported by a majority of the formally employed ‘middle-to-higher’ income earners, their taxpayers benefit from financial support from the Government when they are no longer working. In PNG, the only safety net for the minority of the tax-paying workers is their superannuation savings.

Superannuation savings are for your retirement. In Papua New Guinea, the Income Tax Act sets out how tax is applied when you withdraw your superannuation.

When superannuation is taxed

| Type of contribution | Tax Treatment when in the Fund |

Tax Treatment while in your account |

Tax Treatment when you leave the Fund |

| Employer Contribution | Exempt | Exempt | Taxed (concessional see table below) |

| Employee Contribution |

Exempt (Fund does not tax Employee contribution. Contribution taken from Salary after tax) |

Exempt | Exempt |

| Profit earned by NSL for interest given to Members |

Not derived or paid by Employer or Employee |

Taxed | Taxed (this is the accumulated interest paid by NSL) |

Your Employer's and Employee contribution percentages are calculated on your salary amount, but your employee contribution is deducted on the after tax. You can read more on how superannuation contributions work with your salary and wages tax on the Internal Revenue Commission (IRC)'s website, and read more on the marginal rates here.

While your Superannuation savings are with the Fund, the potential interest that can be earned and applied from the Fund's strategic investments is affected due to tax applied to the profits of its investments. While this does not directly affect your Member and Employer contributions that are with the Fund, the tax does affect the amount of crediting interest that is applied to the Member and Employer contribution balance.

Upon exiting the Fund, under Section 46B of the Income Tax Act 1959, tax is to be applied to all Member benefit payments at the time of exit. Tax is applied only on the Employer and interest component of Members' Super balances. The Member contribution component is not taxed.

Reforms to Tax legislation announced in February 2025 through a National Gazette dictate that, "individuals who have dedicated 15 years or more to service will now enjoy FULL EXEMPTION from tax on their superannuation withdrawals”, and further state that "for Retirement Savings accounts, under the new provision, only the interest earned on these accounts will be taxed, while the principal amount remains entirely untaxed."

Criteria to Access Your Superannuation

- Member must not be working that is formally retired and off the payroll, and;

- Member must be 55 years of age or, Member must have been working with 25 years of service.

- For Members of the disciplinary forces (Royal Papua New Guinea Police Constabulary, Papua New Guinea Correctional Services, and Papua New Guinea Fire Services, Member must be 50 years of age or have been working with 20 years of service.

Reforms to Tax laws on Member benefit payments

In February 2025, the Government announced through a National Gazette:

- Individuals who have dedicated 15 years or more of service will now enjoy FULL EXEMPTION from tax on their superannuation withdrawals.

- For Retirement Savings Accounts (RSA), under the new provision, only the interest earned on these accounts will be taxed, while the principal amount remains entirely untaxed.

What gets taxed?

- Early withdrawals

If you withdraw before 15 years or more of service, only your Employer contributions and Interest will be taxed. Your own contributions (Employee contributions) remain tax free. This is because your income is taxed before your Employee contributions are made. (salary and wages tax rates apply). - Retirement Savings Account

Only the interest earned on RSA accounts will be taxed, while the principal amount remains entirely untaxed.

Comparison of the Superannuation tax before and after the tax reform

| Years of Membership/Contribution | Rate of tax applied BEFORE tax law reform | Rate of tax applied AFTER tax law reform |

| Less than 5 years | Marginal rate of Tax on Employer contributions and accumulated interest |

Not changed |

| 5 years to less than 9 years | The lesser of 15% or the marginal tax rate on the Employer contributions and accumulated interest | Not changed |

| 10 to less than 15 years | The lesser of 8% or the marginal tax rate on Employer contributions and accumulated interest | Not changed |

|

15 years OR under the following circumstance: • Death • Medical • Member is over 50 and has contributed more than 7 years |

2% concessional tax on Employer contributions and accumulated interest |

0% tax on Employer contributions and accumulated interest |

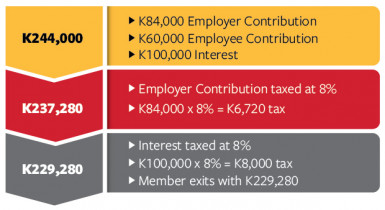

- Let’s assume that a Member has been contributing

to any Superfund for 14 years with K244,000 in

their account when they want to exit. - Under the tax requirements the Member would

qualify for the 8% concessional tax rate.

Tip: If you exit sooner than the legislative

requirements, you will be more impacted by tax.

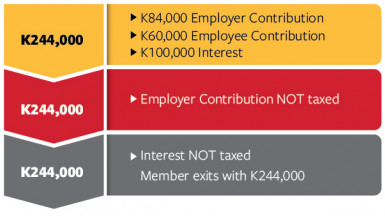

- Let’s assume that the Member has been

contributing to any Superfund for 16 years with

K244,000 in their account when they want to exit. - Under the new tax legislation, the Member would

qualify for the 0% concessional tax rate.

Tip: The longer you contribute, the less tax you pay, or pay NO TAX at all.

To read more on the tax rates and legislation, you can visit the IRC website: https://irc.gov.pg/pages/know-your-taxes/salary-wages-tax